I am struck by the brilliance of the old sentiment, “In the short run, the market is a voting machine, but in the long run it is a weighing machine” from Benjamin Graham, and even more impressed by how it is misused to stop investors trading, or indeed switching advisors.

I always nod sagely, comforted (irrationally) that I and my fund managers are the erudite weighers of stocks, sorting their true value, struck against an eternal benchmark, the assay of perfection.

While the foolish populace run after the ephemeral, the whimsical, the downright corrupt voting machine. But really? Is it not an excuse to hang onto stuff no one wants, a reason to drift along a bit ahead of inflation, a lot behind the market and to talk opaquely about volatility?

The trouble is, the market is the voter, it is the majority personified, it must prevail, worrying about its morals and sanity is largely pointless, if you want to really be richer today than yesterday, or even to just pay your spiralling taxes.

Moats

I am not that convinced either about the guff about compounders and moats, a slight variant, often used for the same purpose to get clients to just sit and hope. It worked very well, as long as the majority of investors believed it, so they voted that way. But when the ballot box shifts, the fundamentals don’t save you.

While the associated aversion to borrowing is good news with rising rates, but a similar burden with falling ones. As for AI, I suspect it is also filling in a fair few of those moats.

Explosive growth

Listening to the India Capital Growth fund manager’s recent talk, available online, I was thrown back into that compounder world, of a pious desire to find gems, and hold them for decades. He will likely underperform, despite a good long run record.

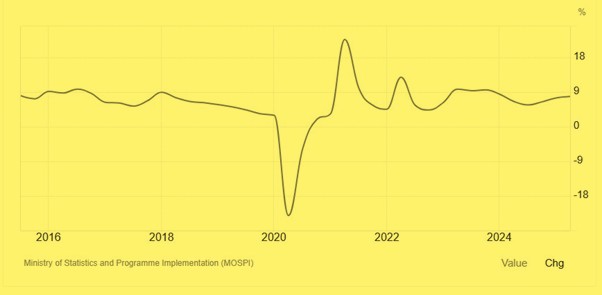

Take the GDP of India in 2015, and place it on the scales, then take the current GDP of India, that is created since 2015, and place that in the pan, on the other side – that provides perfect balance. That’s compounding. Take the output from 5,000 years of a civilisation, add ten years of good government, and globalisation, you just double it. Creating the same again.

India’s GDP growth rate

Yet so far, the Indian market (and that stock) have traded flat/down for a year, in which case the earnings multiple has to be dropping quite fast, so a convincing case exists that it must climb again, in due course.

Yet, I see foreign money (all nicely weighed) leaving India, to be replaced by domestic flows (all voters).

Perhaps the long-term story is fine, but I worry about the coming instability, both internal, as Modi is on the way out, from age alone, and external. Although yet again a thumping win in the Bihar elections, suggests talk of Modi’s demise is premature.

I am concerned less about the global Trump turmoil, which will pass, but the local fund manager, oddly, took exactly the opposite view.

First as a tragedy, then again as a tragedy?

I was reading J.H Huizinga’s essay on The Spirit of the Netherlands, published in a fine English translation in 1968 but written long before, in the 1930’s, when trade and populism were the big threats. Odd how little changes. Back then, to a historian, this was simply obvious. Trade, not territory or ideology is what juices war.

His thought-provoking analysis of political parties was into three groups, “those who acclaim what is, those who acclaim what should be, and those who are determined to make the change”. Or as he puts it conservative, progressive and radical.

He sees no left or right divide on these, the conservative wants to improve, build on, adapt, the progressive to understand, render logical and take to a new state of moral perfection, the radical, to do it all yesterday, regardless of the cost.

The essay is still available, well worth a read. A rejoinder to those who think there is anything new in politics. Any other voter grouping he sees as being a media creation, as all must in time coalesce back into one of the three. To those bleating about fragmentation and five party politics, it provides another lens.

Marching on

So, to markets, fiscal expansion with falling interest rates remains a vital force. You can (as I do) regret how much liquidity is siphoned off into wasteful, unproductive areas, but it was ever thus.

Gold, bitcoin, AI are dominated by the voting machine, running full on, with (at last) the end of the US Government shutdown, removing one significant threat.

At times like these we should be harvesting, locking up returns, reducing risk. But far easier said than done. Looking through my individual stocks, energy feels high, unless Russian and Iranian oil is really off the market, although possibly also, at long last reflecting AI energy demand.

Outside energy and defence, l am not seeing stocks I might want to sell. Nor really am I seeing markets I wish to exit.

Big banks and insurers are perhaps moving to be fairly valued, despite quite staggering rises, as they were just far too cheap. Other financials still look cheap, as perennially does property.

But overall, there is not a great deal you would actively sell. Most are sitting above my buy floor, but well below my sell ceiling, except to rebalance portfolios. This is what is needed, but it seems an oddly mechanistic approach, to sell cheap, because you have too much. Nor is it one that ever brings much satisfaction.

Perhaps I then just buy more of the right ‘weight’, that a marketplace of ‘voters’ will still continue to ignore.