We take a look out from the COVID saga, and bubbles are apparent, but fiscal expansion and falling rates persist.

Fuel for the fire

The extraordinary COVID crisis saw everything shut down, except fresh government borrowing, then everything was released, government borrowing continued, and that extended surge remains, fuelled by falling interest rates. A remarkably fertile combination.

Added to that sectors of the world are seeing accelerated debt fuelled capital spend, part AI driven, part replacing capacity that was lost to COVID or Putin or Xi or Trump.

A world in which we were all gliding to the lowest cost global producer has now ended. Instead, we see the destruction of excess low-cost capital and its replacement being built behind tariff and sanction walls.

Much of the destruction is happening in places with no viable capital markets, but most of the value creation is in places with very active markets.

Not all, the slowing of ESG, the advance of AI, the new protectionism, are destroying traditional auto manufactures, steel plants, turbine manufacturers, advertising agencies, and the assumption is it will tear through professional services too.

But much of the destruction is still happening off camera.

While the failure by Central Banks (again) to control inflation, along with governments desperately trying to halt their rising debt mountains, has left the new normal interest rates higher than most expected.

Chart showing interest rates of different countries below

What is burning

What does this then look like? In aggregate there is no bubble, inflation adjusted, most markets this century are pretty dull. A long run real return has been elusive.

We would expect that: COVID, Ukraine, even back to the Great Financial Crisis, have all been destroyers, not creators.

For now, it all helps America. There is no angst about state debt levels in the White House, they have the leadership in AI, they have the tech giants to distribute it and build cloud storage, we have given them deep capital markets to fund it, they have shale oil, and no concerns about burning coal (or nuclear) to impede them, they have a military strong enough to stay out of wars, well-armed enough to fight distant foes by local proxy, and added to that both the global reserve currency, a lot of the crypto wealth, which they welcome, and now a tariff wall, so their own market can be served at short range, by domestic producers.

Short term, it all looks rather good for them, and in markets they already dominate. The US is cleverly attacking other powers with sanctions, of one sort or another, covering the majority of the globe, and its historic competitor, Europe, spends its time knitting new shackles to stifle movement, while, it seems, still hoping to single handedly save the planet.

So perhaps the question for the US market is what took so long, rather than is this a bubble?

Yet it is a bubble, AI valuations are assuming all the upside.

However, America has to be less productive, behind tariff walls, and creating redundant high price capital on a grand scale, while funding a spiralling debt burden.

It looks like a race between all those positives and an inevitable decline.

Yin and yang

Bitcoin has done well, gold exceptionally well, anything tech related looks hot, despite nerves over some software. Energy is climbing too, based on the assumed endless hunger of AI.

While value is a mixed bag. As rate cut hopes have faded, a number of high yielding stocks have fallen back, in particular the classic geared plays of property and private equity. Neither has done much this year, and dollar weakness has further eroded returns for UK investors. Although PE is well clear of its pre-COVID level, property is still struggling below that. In both cases interest rate expectations dominate.

The more you pay lenders the less you pay owners – it is that simple.

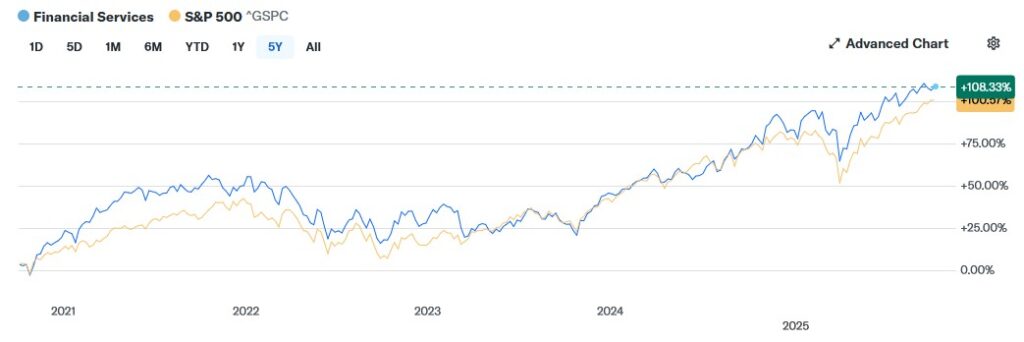

While the big financial firms have done very well, on a mix of interest rates staying high, but low demand and falling rate expectations, letting their deposit costs drift down. Markets saw high interest rates as a peak, not as a plateau, and as the elevated interest rates remain and buy backs roll ever forward, so the share prices climb higher.

The following is a chart of the performance of the financial services sector stocks, in blue against the S&P shown in yelow.

Stasis

Which brings us to politics, which having hit rock bottom, in the public eye, has nervously settled there.

Neither Reform, nor its supporters can really believe it will win in the UK, while the very prospect sends tremors through the establishment.

The (very slowly) dawning realisation that their own electoral promises are unfundable continues to gnaw at ruling parties, just as it encourages their opponents.

I think it is all noise, until we get a real election, still a long way off here.

I believe Starmer is secure, I don’t see a better navigator of the chaos on Labour benches – I guess that means Rachel from Accounts is too. Kemi Badenoch has bigger problems, doing the right thing turns lukewarm supporters into lukewarm opponents, the party has grown lazy in its ambition, loaded with admirals and not enough ships. A further drubbing by Reform seems inevitable, and I am sure she can hold her nerve, but can the party?

So, I see good macro reasons for markets being too low, but only in sectors where global investors are interested. Takeovers still feel muzzled by political interference, although all the unloved sectors are seeing spare capacity taken out.

But there still look to be bargains. So that headbanging, everything-has-gone-up, signal of a bursting bubble is not visible.

So, I see no reason for more than a typical annual correction.

A fundamental shift needs more radical news.